Resources

Insights From HealthJoy

Insights From HealthJoy

Curated resources, insights, and perspectives from the HealthJoy team, built for benefits leaders, consultants, and the people shaping healthcare today.

Curated resources, insights, and perspectives from the HealthJoy team, built for benefits leaders, consultants, and the people shaping healthcare today.

Blog Post

The Gen Z Warning: Why Your Youngest Employees Are Sending an Early Signal

Rising prescription costs among the youngest members of a workforce should prompt a specific question: why are members in their early twenties needing more medication than they did a year ago?

·

Landing Page

The Predictive Advantage: Leveraging Real-Time Member Intent to Control 2027 Costs

·

Landing Page

Get on the priority list for HealthJoy’s newest products

·

Press

HealthJoy's Benefits Operating System Drives 18% Savings on Medical Procedures Through Intelligent Steerage

Independent analysis confirms HealthJoy saves $327 per employee per year by influencing heavy utilizers and high-volume care categories

HealthJoy

·

Blog Post

More Good Days, Together: Why Solving Chronic Pain is a Key Part of Your Mental Health Strategy

May is Mental Health Awareness Month. It’s a moment when employers, HR teams, and benefits leaders turn their attention to the emotional wellbeing of their workforce. But if your mental health strategy starts and ends with mental health benefits, you may be missing one of the most powerful levers you have.

HealthJoy

·

Webinar

On Demand: From Navigation to Orchestration: What's Next for HealthJoy's Benefits Operating System, on demand

HealthJoy is pioneering a new era of benefits: end-to-end orchestration. Watch our webinar as we reintroduce HealthJoy’s Benefits Operating System: the platform that connects benefits strategy to the decisions employees actually make, from enrollment through every care decision across the full plan year.

HealthJoy

·

Blog Post

From Navigation to Orchestration: Closing the Gap Between Benefits Strategy and Employee Decision

Benefits have always had a strategy. It's never had a system. Here's why HealthJoy is changing that, and what end-to-end benefits orchestration means.

Brian Astrachan

·

Blog Post

The Millennial Cancer Surge: Why Your “Low-Risk” Population Is Your Newest Liability

Data from HealthJoy’s 2026 Member Health Goals Report reveals a troubling shift that demands attention before your next renewal: cancer diagnoses among members aged 26–35 surged 25% in just one year.

HealthJoy

·

Blog Post

The 12-Month Warning: Your Members Are Already Telling You What Your 2027 Claims Will Look Like

Most benefits strategies are built on a data signal that arrives too late to change outcomes. Claims data is the most available signal for managing population health risk, but it's a lagging one.

HealthJoy

·

Blog Post

The GLP-1 Policy Gap: What Every Employer Needs to Build Before Their Next Renewal

According to HealthJoy’s 2026 Member Health Goals report, nearly 60% of members have expressed weight loss intent. That’s not a fringe population. That’s the majority of your workforce quietly calculating whether their benefits will cover what they want and what their providers are increasingly willing to prescribe.

HealthJoy

·

Report

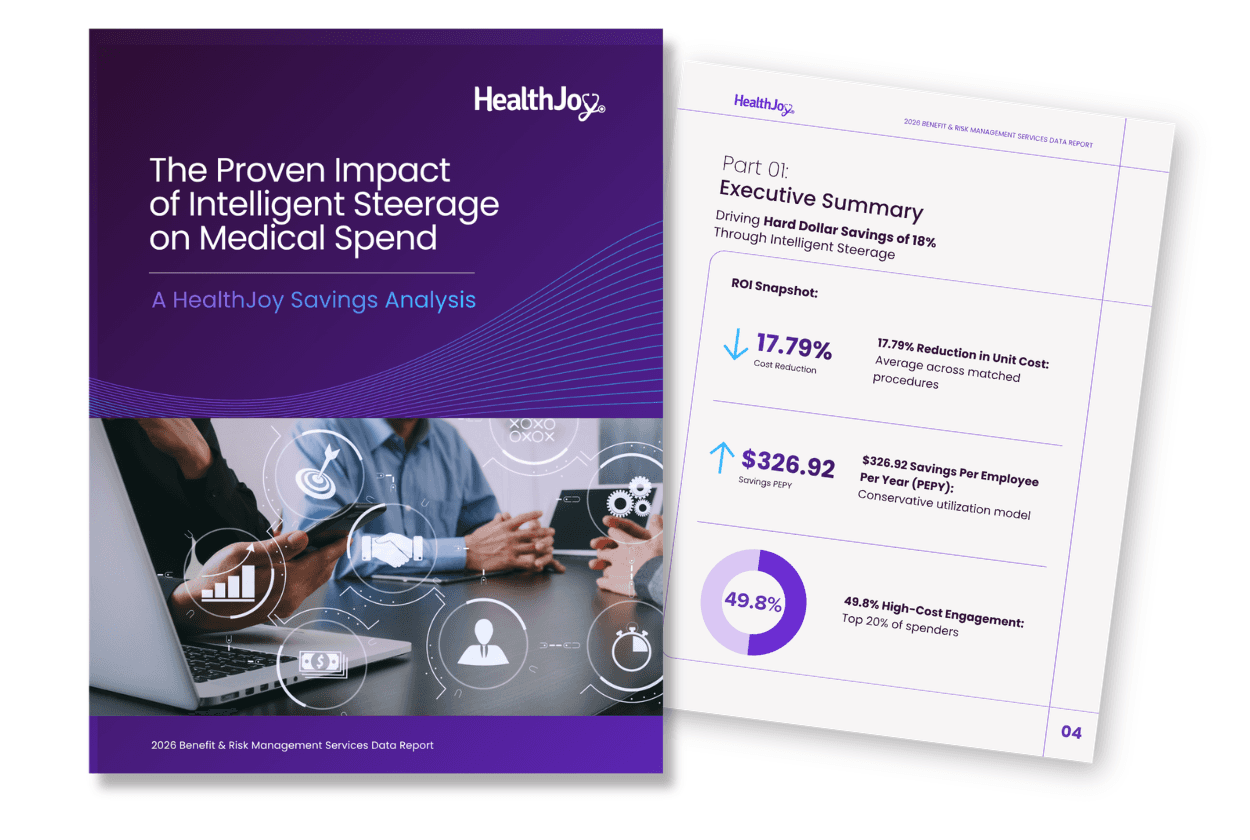

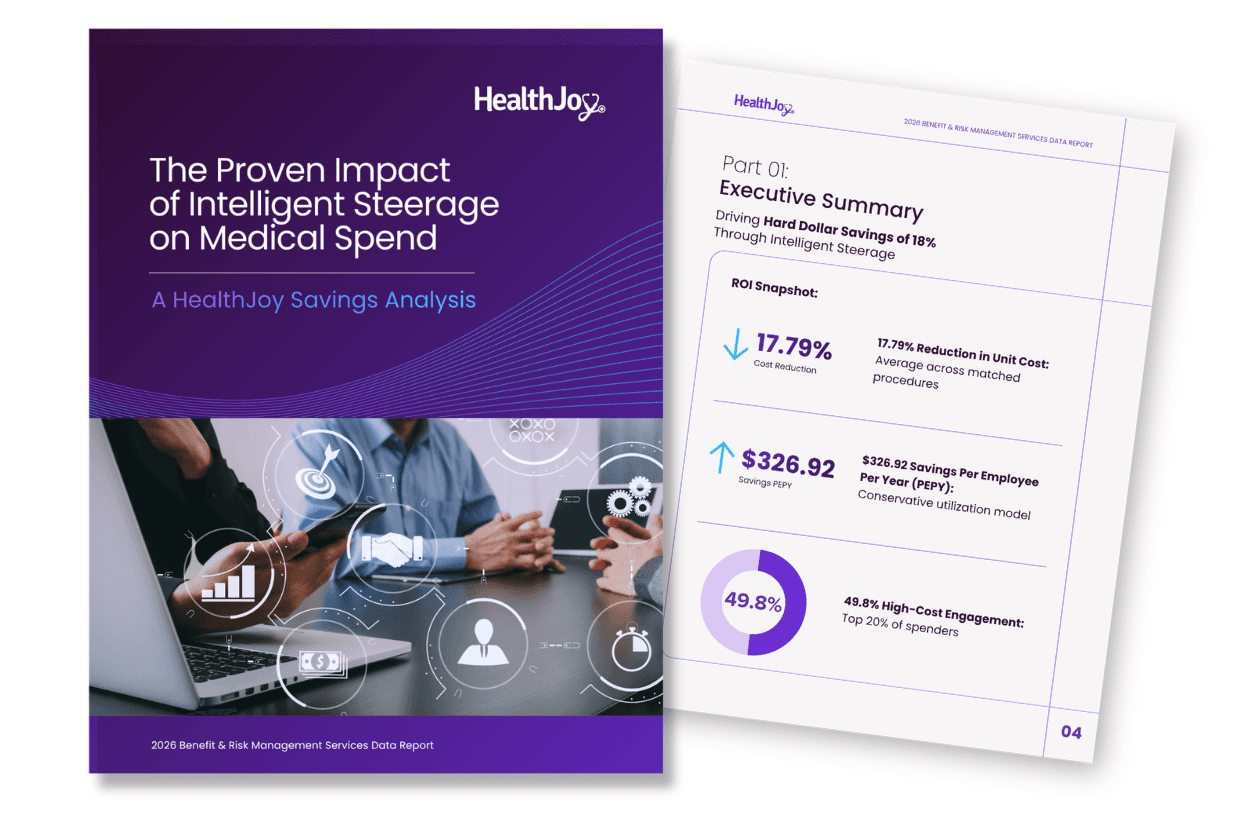

The Impact of Intelligent Steerage on Medical Spend: A HealthJoy Savings Analysis

This third-party validated report quantifies what that navigation gap costs and what happens when it's closed. By matching HealthJoy-guided claims against an identical control group, procedure by procedure, we isolated the true price difference between guided and unguided care.

HealthJoy

·

Report

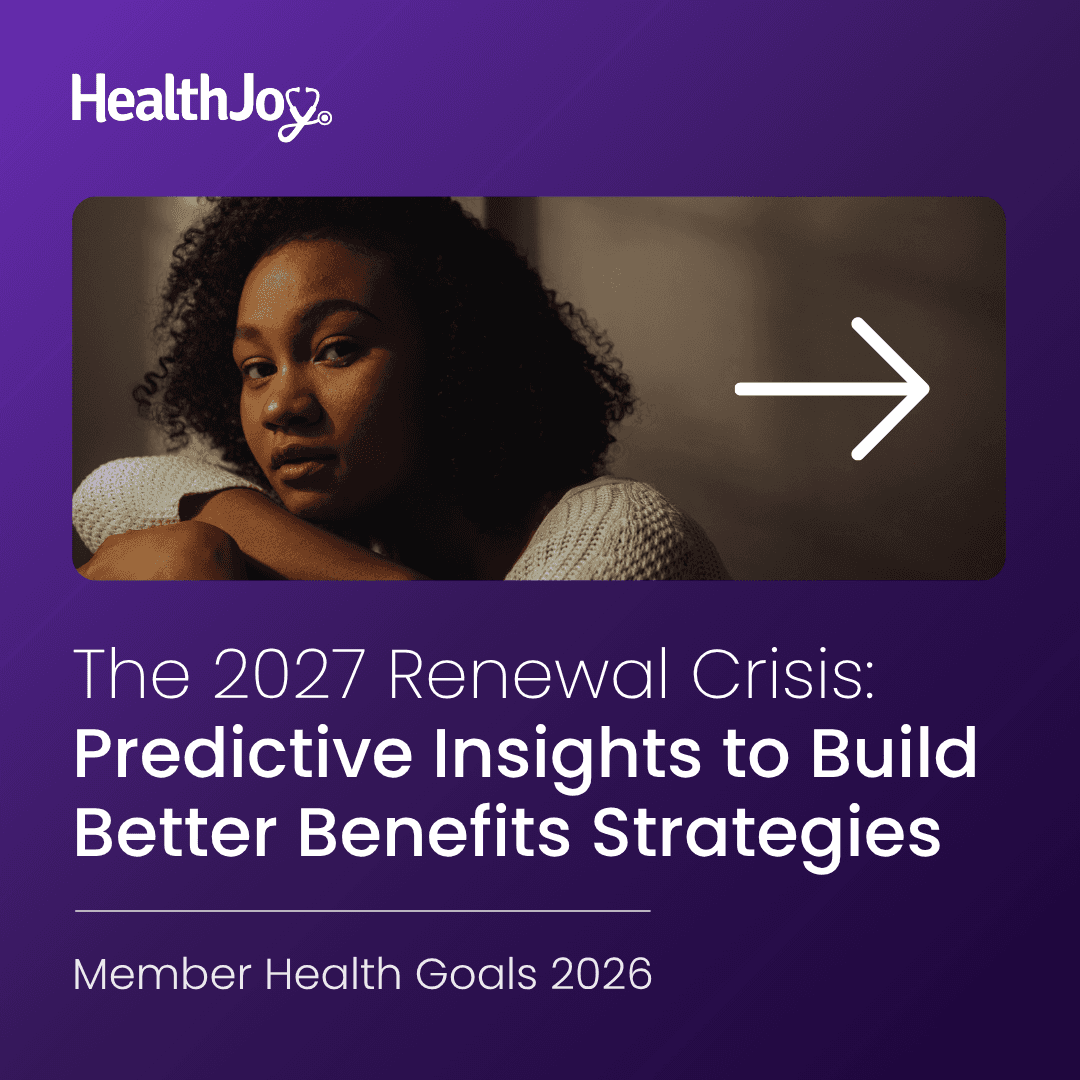

The 2027 Renewal Crisis: Predictive Insights to Build Better Benefits Strategies

For the fourth year in a row, HealthJoy's Member Health Goals report translates what your members are telling us right now into the data that claims reports can't show you: self-reported health intent from over 100,000 members.

HealthJoy

·

Press

HealthJoy Moves Beyond Navigation to One End-to-End Benefits Operating System

New capabilities guiding enrollment, wellness, and healthcare decisions aim to drive high-value care year round

HealthJoy

·

Blog Post

Navigation Gets Members to the Door. Incentives Get Them Through It.

The Benefits OS finds the right provider. HealthJoy Incentives makes sure members choose it. And you only pay when savings are real.

Brian Astrachan

·

Blog Post

The Gen Z Warning: Why Your Youngest Employees Are Sending an Early Signal

Rising prescription costs among the youngest members of a workforce should prompt a specific question: why are members in their early twenties needing more medication than they did a year ago?

·

Blog Post

The Millennial Cancer Surge: Why Your “Low-Risk” Population Is Your Newest Liability

Data from HealthJoy’s 2026 Member Health Goals Report reveals a troubling shift that demands attention before your next renewal: cancer diagnoses among members aged 26–35 surged 25% in just one year.

HealthJoy

·

Landing Page

The Predictive Advantage: Leveraging Real-Time Member Intent to Control 2027 Costs

·

Blog Post

The 12-Month Warning: Your Members Are Already Telling You What Your 2027 Claims Will Look Like

Most benefits strategies are built on a data signal that arrives too late to change outcomes. Claims data is the most available signal for managing population health risk, but it's a lagging one.

HealthJoy

·

Landing Page

Get on the priority list for HealthJoy’s newest products

·

Blog Post

The GLP-1 Policy Gap: What Every Employer Needs to Build Before Their Next Renewal

According to HealthJoy’s 2026 Member Health Goals report, nearly 60% of members have expressed weight loss intent. That’s not a fringe population. That’s the majority of your workforce quietly calculating whether their benefits will cover what they want and what their providers are increasingly willing to prescribe.

HealthJoy

·

Press

HealthJoy's Benefits Operating System Drives 18% Savings on Medical Procedures Through Intelligent Steerage

Independent analysis confirms HealthJoy saves $327 per employee per year by influencing heavy utilizers and high-volume care categories

HealthJoy

·

Report

The Impact of Intelligent Steerage on Medical Spend: A HealthJoy Savings Analysis

This third-party validated report quantifies what that navigation gap costs and what happens when it's closed. By matching HealthJoy-guided claims against an identical control group, procedure by procedure, we isolated the true price difference between guided and unguided care.

HealthJoy

·

Blog Post

More Good Days, Together: Why Solving Chronic Pain is a Key Part of Your Mental Health Strategy

May is Mental Health Awareness Month. It’s a moment when employers, HR teams, and benefits leaders turn their attention to the emotional wellbeing of their workforce. But if your mental health strategy starts and ends with mental health benefits, you may be missing one of the most powerful levers you have.

HealthJoy

·

Report

The 2027 Renewal Crisis: Predictive Insights to Build Better Benefits Strategies

For the fourth year in a row, HealthJoy's Member Health Goals report translates what your members are telling us right now into the data that claims reports can't show you: self-reported health intent from over 100,000 members.

HealthJoy

·

Webinar

On Demand: From Navigation to Orchestration: What's Next for HealthJoy's Benefits Operating System, on demand

HealthJoy is pioneering a new era of benefits: end-to-end orchestration. Watch our webinar as we reintroduce HealthJoy’s Benefits Operating System: the platform that connects benefits strategy to the decisions employees actually make, from enrollment through every care decision across the full plan year.

HealthJoy

·

Press

HealthJoy Moves Beyond Navigation to One End-to-End Benefits Operating System

New capabilities guiding enrollment, wellness, and healthcare decisions aim to drive high-value care year round

HealthJoy

·

Blog Post

From Navigation to Orchestration: Closing the Gap Between Benefits Strategy and Employee Decision

Benefits have always had a strategy. It's never had a system. Here's why HealthJoy is changing that, and what end-to-end benefits orchestration means.

Brian Astrachan

·

Blog Post

Navigation Gets Members to the Door. Incentives Get Them Through It.

The Benefits OS finds the right provider. HealthJoy Incentives makes sure members choose it. And you only pay when savings are real.

Brian Astrachan

·

The Benefits Operating System, connecting your entire benefits ecosystem into one intelligent platform.

© 2026 HealthJoy. All rights reserved.

The Benefits Operating System, connecting your entire benefits ecosystem into one intelligent platform.

© 2026 HealthJoy. All rights reserved.

The Benefits Operating System, connecting your entire benefits ecosystem into one intelligent platform.

© 2026 HealthJoy. All rights reserved.